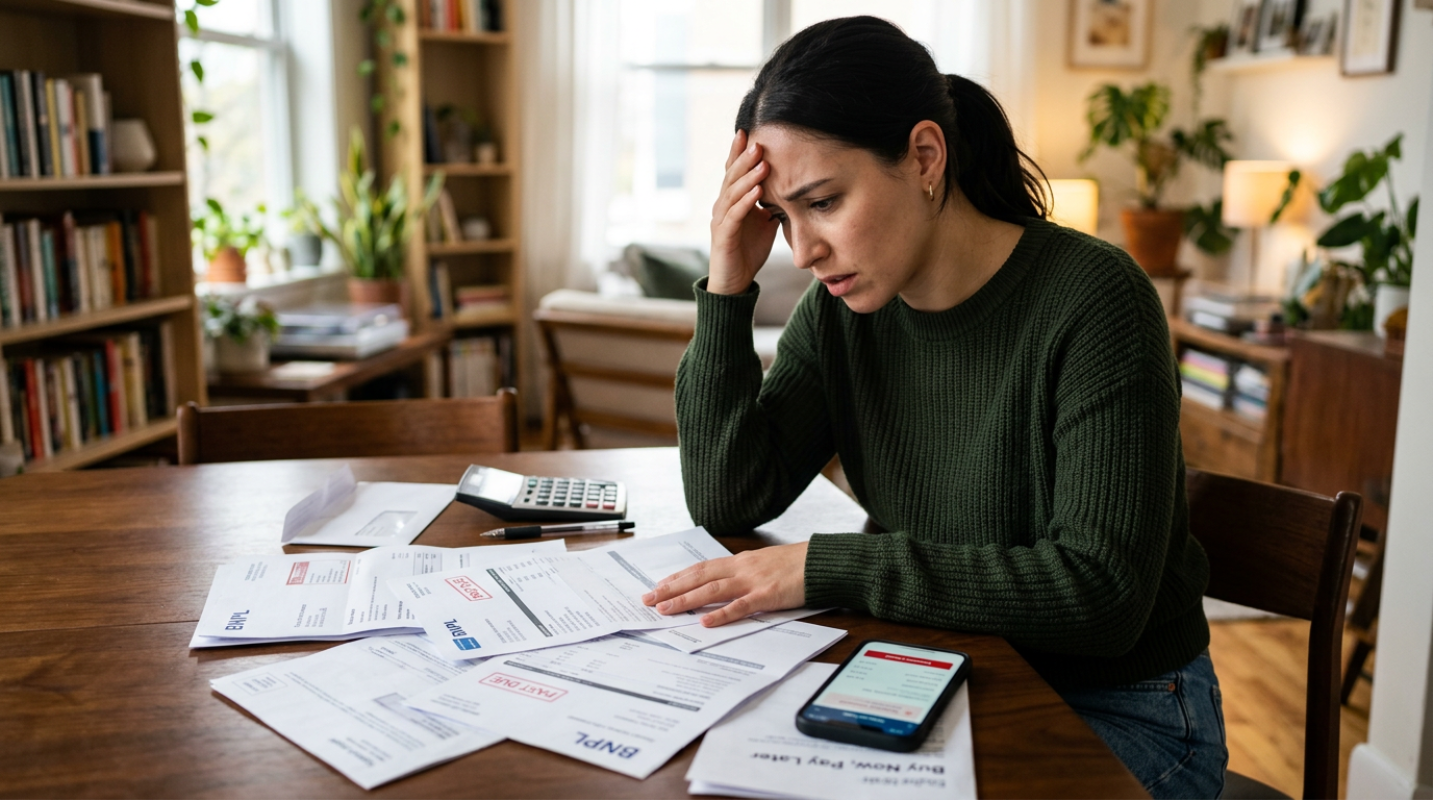

Let's face it. Living paycheck to paycheck is exhausting. When you are scraping by, the advice to save three to six months of expenses sounds like a cruel joke. How are you supposed to save thousands of dollars when you can barely cover rent?

If you feel this way, you are far from alone. According to Bankrate's 2026 Emergency Savings Report, 53% of Americans cannot cover an unexpected $1,000 expense from savings alone.¹ The Federal Reserve's latest data shows a similar struggle, with 37% of adults unable to cover a sudden $400 emergency using cash.²

But an emergency fund is not a luxury for the wealthy. It is a tool for peace of mind. It is the only thing standing between you and a high-interest debt spiral when your car breaks down or your hours get cut. You do not need a massive pile of cash to start. You just need a plan to build momentum.

Mastering Budgeting on a Low Income

When money is tight, you have to know exactly where every single dollar goes. It is easy to ignore your bank account when looking at it causes anxiety. But ignoring the numbers will not make them go away. Facing your finances head-on is the first step toward taking back control.

Start by tracking your spending for just two weeks. Use a free app or a simple paper notebook. You might find hidden leaks, like a subscription you forgot to cancel or daily convenience purchases that add up. Once you see where the money goes, you can make conscious choices about where it should go instead.

Next, separate your needs from your wants. During tight periods, needs are strictly survival: housing, basic groceries, utilities, and transportation. Everything else is a want. This does not mean you can never have fun, but it means those wants must take a back seat while you build your safety net.

The traditional 50/30/20 budget (50% needs, 30% wants, 20% savings) does not work when your needs consume 80% of your income. Instead, modify it. Try an 80/10/10 split, or even 90/5/5. The exact percentages do not matter as much as the act of intentionally assigning a job to every dollar.

Micro-Savings Approaches That Actually Work

If you cannot save $100 a month, can you save $5 a week? What about $10?

Starting small is the secret to building a saving habit. When you prove to yourself that you can save $5 a week, you build the psychological momentum needed to save more later. It shifts your mindset from survival mode to planning mode.

To make this work, you need to make saving invisible. Here are three ways to do it

• Round-up apps: Use tools that automatically round up your debit card purchases to the nearest dollar and slide the change into savings. It is the digital equivalent of a spare change jar.

• Automated transfers: Set up a recurring transfer of $5 or $10 from your checking account to your savings account on the day you get paid. If you do not see the money, you will not miss it.

• The bill trick: Treat your savings like a non-negotiable monthly bill. You would not ignore your electric bill, so do not ignore your future self.

Optimizing Your Financial Cushion

Where you keep your money matters just as much as how much you save. Keeping your emergency cash in your everyday checking account is a recipe for accidental spending.

Instead, move your money to an online High-Yield Savings Account (HYSA). Traditional brick-and-mortar banks pay an average of 0.39% interest, but many HYSAs pay over 4%. Letting compound interest do some of the heavy lifting is free money.

For those with fluctuating hours, gig work, or seasonal jobs, a single emergency fund might not be enough. Financial planners recommend building a buffer account alongside your core emergency fund. During higher-earning months, put extra cash into the buffer. During low-earning months, draw from the buffer to pay regular bills, leaving your core emergency fund untouched.

What about debt? Many financial experts advise paying off credit cards before saving. But if you have zero savings, any emergency will send you right back to using credit cards. The smarter move is to pay only the minimums on your debt until you secure a starter emergency fund of $1,000. Once you have that cushion, you can tackle your debt with real peace of mind.

Finding Extra Room in a Stretched Budget

When your budget is already stretched to its limit, you have to get creative to find extra cash.

Start by hunting down phantom expenses. These are the small, forgotten costs that quietly drain your account. Cancel the streaming service you only watch once a month. Call your car insurance company and ask for a higher deductible to lower your monthly premium.

Next, look at windfalls. If you get a tax refund, a small cash gift, or cash-back rewards from apps, do not spend them. Put at least half of that money directly into your emergency fund. Because this cash is outside your normal paycheck, saving it will not hurt your day-to-day lifestyle.

You can also generate quick cash by selling unused items around your home or taking on a temporary side hustle. Think of this as a short-term sacrifice for long-term security. Selling an old phone or working a few extra hours for a month can fully fund your starter safety net.

Finally, do not hesitate to use community resources or government assistance programs. Programs like SNAP for groceries or LIHEAP for utility bills are tools designed to help you get by. Using them frees up the breathing room you need to start saving.

Consistency Over Intensity

You do not need to reach your ultimate savings goal overnight. In fact, trying to save too fast can lead to a cycle of saving and then immediately withdrawing the money when you run short.

Focus on small milestones instead. A landmark Vanguard study found that having just $2,000 in emergency savings is the single strongest predictor of financial well-being.³ The researchers call this the desert water rule. Just like a small cup of water saves your life in a desert, a $2,000 buffer provides a massive boost to your peace of mind.

Other researchers have found that $2,467 is the best minimum goal to keep low-income families out of high-interest debt cycles.

Do not let the big numbers scare you. Every dollar you save is a victory. Stay consistent, start small, and watch your safety net grow.

Sources:

1. Bankrate's 2026 Emergency Savings Report

https://www.bankrate.com/banking/savings/emergency-savings-report/

2. Federal Reserve Survey of Household Economics and Decisionmaking

https://www.federalreserve.gov/consumerscommunities/sheddataviz/unexpectedexpenses-table.html

3. Vanguard Emergency Savings Study

https://corporate.vanguard.com/content/corporatesite/us/en/corp/articles/emergency-savings-may-hold-key-financial-well-being.html

*This article on infotable is for informational and educational purposes only. Readers are encouraged to consult qualified professionals and verify details with official sources before making decisions. This content does not constitute professional advice.*

.png)