(Image source: Gemini)

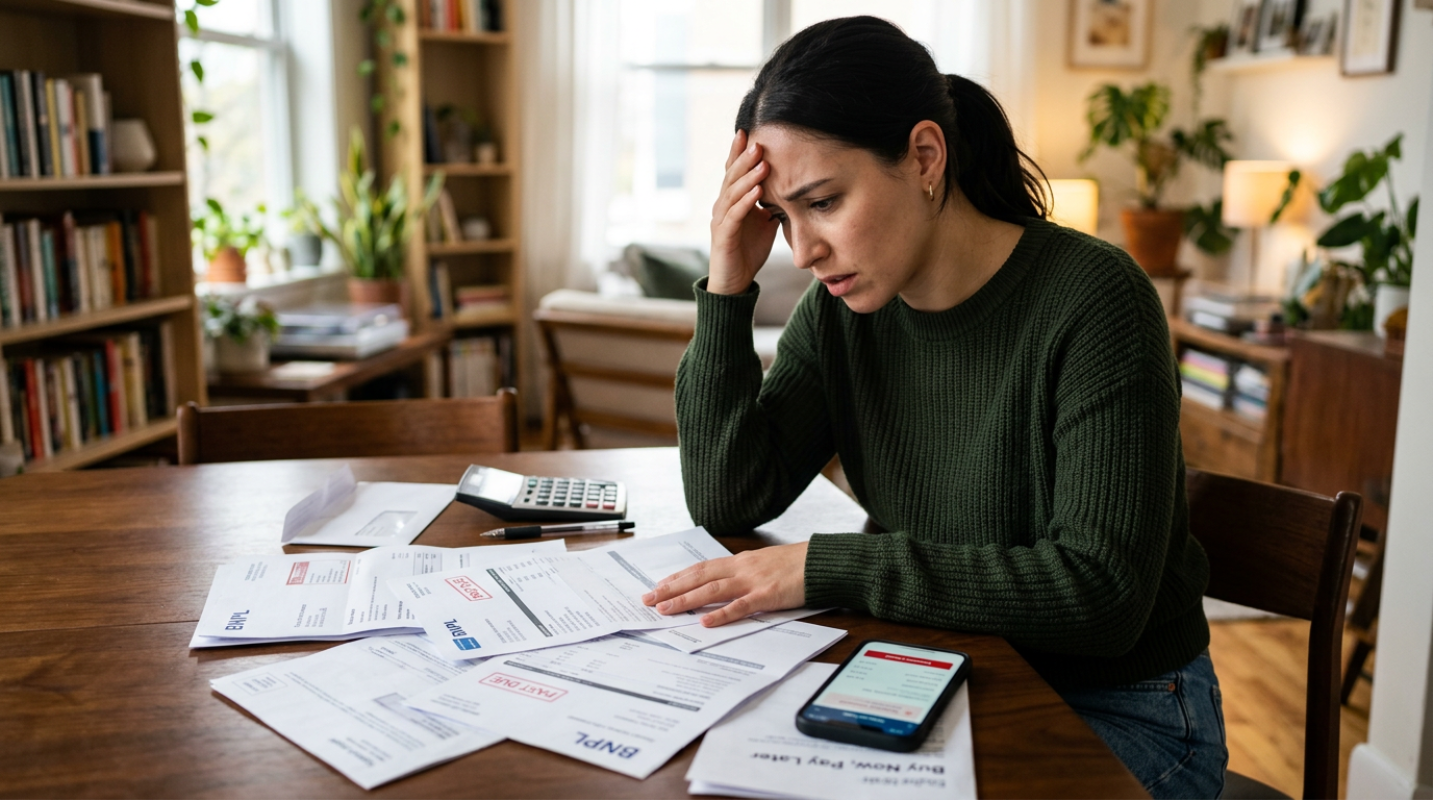

(Image source: Gemini) You've seen the button at checkout. It's usually a bright, friendly color, promising to turn that $400 purchase into four "easy" payments of $100. It feels like a win. You get the item today, and your bank account doesn't take the full hit until next month. But this frictionless experience is exactly what makes Buy-Now-Pay-Later (BNPL) so deceptive. It masks the reality that you're taking out a loan, often without the friction that usually makes us stop and think.

By early 2026, the U.S. market for these mini-loans will have reached a staggering $70 billion. It's grown at a massive 20% clip every year since 2021. Why? Because it's easy. It's the digital equivalent of a smooth-talking salesperson who tells you not to worry about the price tag. This shift in consumer behavior is moving away from traditional credit cards, which have clear monthly statements, toward a fragmented mess of tiny installment plans scattered across half a dozen different apps.

The psychological trick here is what experts call the "payment separation effect." When you break a cost into pieces, your brain treats the smaller number as the "real" cost. You aren't spending $200. You're just spending $50. But when you do that ten times across different stores, you've suddenly committed $500 of your future income before you've even paid your rent. Have you ever looked at your bank statement and wondered where all the money went, only to find five different $40 deductions you forgot about? That's the trap.

The Data Behind the Surge in Defaults

If you look at the official reports from big banks, things might look okay on the surface. As of early 2025, BNPL charge-off rates (the actual defaults companies write off) were around 2%. That's much lower than the 10% average for credit cards. But this is where the data gets sneaky. Although actual defaults are low, the number of people struggling to keep up is skyrocketing.

By the middle of 2025, data showed that 41% of BNPL users missed at least one payment in the previous year.¹ That's a huge jump from the 34% we saw in 2023. So, why aren't the "default" numbers higher? It's because of "phantom debt." Most BNPL providers don't report your on-time payments or your total balances to the big credit bureaus like Experian or TransUnion. This means your debt-to-income ratio looks healthy to a traditional lender, even if you're drowning in installment payments.

This visibility gap is a systemic problem. Wells Fargo economists called this an "unregulated danger zone" late last year. Because there's no central tracking system, you can "stack" loans. You can have an open balance with Affirm, another with Klarna, and a third with Afterpay, all at the same time. None of those companies knows about the others. It's like a bartender serving you a drink because you don't have a tab open at their bar, completely unaware that you've already had five drinks at the place next door.

Consumers are Struggling

Life has gotten expensive. Inflation and the rising cost of living have put a massive strain on household budgets over the last few years. When the price of eggs, gas, and insurance goes up, something has to give. For many, BNPL has shifted from a way to buy a new pair of sneakers to a way to survive the week.

A really telling trend in 2025 was the migration of BNPL into "needs" rather than "wants." By mid-2025, 25% of users were using these plans to buy groceries. A year prior, that number was only 14%. When you're financing your milk and bread, that's a sign of extreme financial stress. It's effectively using BNPL as a high-frequency payday loan substitute, but without the same level of scrutiny.

Younger generations are at the epicenter of this mess. Gen Z users are struggling the most, with 57% of them reporting a missed payment by the end of 2025. Many of these users are subprime borrowers who are already maxing out their credit cards. When you layer BNPL debt on top of credit card utilization rates that are already hitting 60%, you're looking at a ticking time bomb. If you lose your job or have an emergency, those automated payments will keep hitting your debit card, triggering a chain reaction of overdraft fees and leaving you with nothing for rent.

The Regulatory Gap

For a long time, BNPL companies operated in a bit of a Wild West. They argued they weren't "credit" in the traditional sense because they didn't always charge interest. But in May 2024, the Consumer Financial Protection Bureau (CFPB) stepped in. They officially classified these providers as credit card providers, which meant they finally had to offer things like dispute protections and refund rights.

But since then, we've seen a bit of a "regulatory lag." As we move through 2026, there's a concern that the push for stricter oversight has slowed down. This is happening just as delinquency rates are peaking. Although companies like Affirm argue that their model is safer because it's not "refinancing" debt that compounds forever, the reality of loan stacking remains a massive risk.²

What do the experts see for the rest of 2026? Most predict a significant tightening of credit. As defaults and late payments climb, these platforms will likely become more selective about who they lend to. We'll probably see a push for better transparency and perhaps even a centralized reporting system so lenders can see the "phantom debt" before they approve another purchase. But until then, the burden of protection is mostly on you.

Managing Your Debt

If you find yourself juggling multiple payments, it's time to take a step back and look at the big picture. It's easy to lose track when the amounts are small, but they add up to a heavy weight on your shoulders.

- Audit your apps: Open every single BNPL app on your phone and write down exactly what you owe and when it's due. You might be surprised by the total.

- Prioritize high-fee loans: Not all BNPL plans are equal. Some have flat late fees, while others might impact your ability to use the service again. Pay off the ones that cost you the most first.

- Watch your bank balance: Since these apps usually pull money directly from your debit card, they can cause a series of overdraft fees if you aren't careful. Turn off "autopay" if you need to control exactly when the money leaves your account, but be careful not to miss the deadline.

- Seek help early: If you're using BNPL for needs like groceries or utility bills, it's a sign that your budget is broken. Don't wait for a total default. Talk to a non-profit credit counselor who can help you consolidate your debt.

Taking Control of Your Wallet

The "climb" in credit defaults isn't always obvious because it's hidden in the fine print of app-based lending. Although the big banks might look stable, the average person's bank account is telling a different story. BNPL isn't inherently evil, but it's a tool that's very easy to misuse. It's designed to make you spend more than you intended by making the cost feel smaller than it is.

So, what's the move? It's about being honest with yourself. If you can't afford the item today, can you really afford it in four weeks? Most of the time, the answer is no. By recognizing the psychological tricks and the "phantom debt" risks, you can make sure you're using these tools to your advantage rather than letting them use you. Don't let a "frictionless" checkout turn into a long-term financial headache.

This article on infotable.co is for informational and educational purposes only. Readers are encouraged to consult qualified professionals and verify details with official sources before making decisions. This content does not constitute professional advice.

.png)